Technology is changing the playing fields in business – and in the financial planning environment in particular, can allow intermediaries to enhance their business operations and their client engagement. On the other hand, the human element is similarly important – for insight, holistic thinking and a trusted relationship. Optimally combining the two, in a well-considered and complementary way, can mean greater efficiency, greater productivity and more satisfied clients. But the key is to get it right. This is according to Jacques Coetzer, General Manager of Sanlam Broker Distribution.

”The opportunity sits in catering for clients’ digital requirements while moving to a world where people may increasingly require human interaction. In the US and globally, we are seeing new financial intermediaries emerge as financial coaches. Alongside a service interaction, clients are asking for coaching and support in their decision making. In a time of economic turbulence and information saturation, on-going empathetic guidance in line with a holistic big-picture approach goes a long way to cementing a client relationship based on trust.”

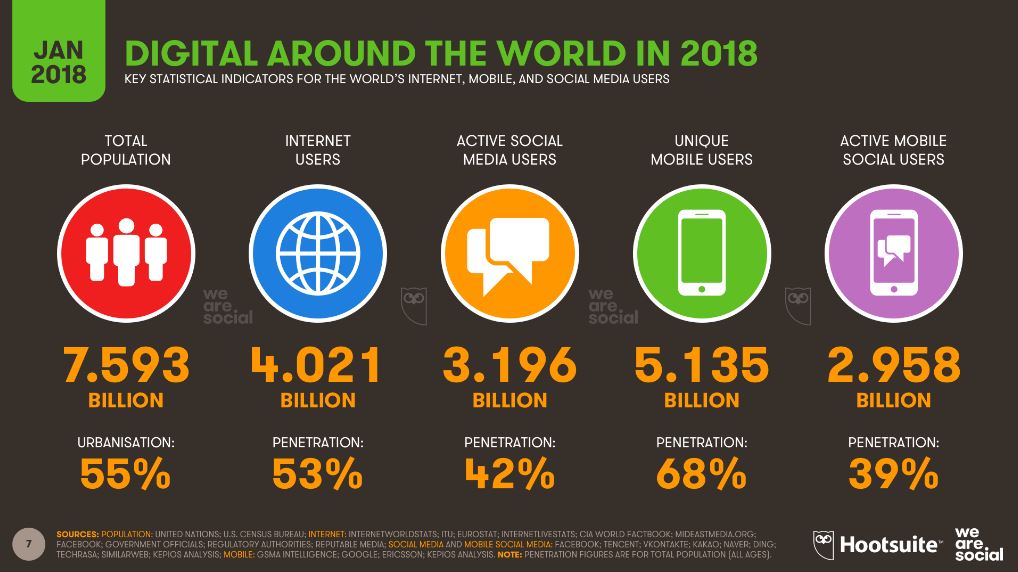

Against this backdrop, Coetzer says clients are increasingly seeking an omni-enabled experience which positions convenience as a norm, and not an accolade. The University of Stuttgart predicts that by 2020, 40% of financial services-focused interactions by intermediated clients will be digital “Think of the transformation catalysed by online banking. If you don’t have to queue in a branch, why would you? To stay relevant, intermediaries will need to carefully consider how to integrate consumer-facing technologies to the benefit of their clients.”

Coetzer says many intermediaries and businesses will find the planning and implementing of the transition to a more digital-led approach, daunting. The biggest barriers are usually resistance to change, lack of resources, or in some cases, understanding of what needs to be done. As a start, here are some recommendations of how technology can reinforce a relationship with a client. It is certainly not an exhaustive list, but is a good start for intermediaries:

- Offer pre-emptive communication on a preferred platform: If something big happens (like the Minister of Finance’s National Budget speech) consider pre-emptively emailing clients to guide them on the implications for their personal finances. You could even send them a WhatsApp broadcast. The point is to be on-hand and to communicate on the platforms on which clients are most active.

- Get to know clients on a granular level by tapping into their data: Big data may be a buzzword, but simply put, it’s providing psychographic information on an unprecedented scale. Use your website and other electronic means to gather fresh data about your client, their preferences and personal circumstances. If your clients feel comfortable sharing some of that information with you, it could catalyse more in-depth profiling so that you can offer better advice and a selection of the most relevant products.

- Use automation and other technology tricks to up your value: By automating some of your administrative tasks, you could invest more time in client relationships. Additionally, technology streamlines interactions and enhances client experiences, thereby becoming an important value-add. People’s most valuable commodity is time, so saving it is bound to offer significant benefits to clients. It may be worth speaking to a technology consultant to find out what tasks in your business can be automated. In particular to free up the time of those individuals who should be spending their time with clients.

- There’s room for technology as well as the human element: While the proliferation of robo-advice proves its success as a powerful business tool, many FinTechs linked to purchasing products are aimed at single needs, leaving room for a financial adviser to offer a more integrated view and coaching.

- Not only millennials use technology: In 2017, UK research showed very little difference between baby boomers and millennials in their preference for digital service. Clients across the board are seeking convenience, so your digital solutions need to cater for everybody.

There is no uniform approach that will suit all intermediaries, so it is important to find the technology solutions that best suit your business. Coetzer says ultimately technology should be used to deepen an existing relationship by personalising advice and honing the convenience factor.

In addition, it is crucial for product providers to be highly present in the digital market place. So often, the perception is that when product providers implement technology for clients to self-service, it aims to disintermediate the intermediary. However, if done correctly, it actually has the opposite effect and generate leads for intermediaries instead. From the product provider’s perspective, digital online fulfilment does not mean detracting from the role or value of an intermediary. Companies have to be digitally present, because if they are not, clients could easily choose to buy elsewhere. When a client buys a product online, and the service and process adds value to them, a digital trust relationship is created – and helps the business to add further value to the client by offering holistic financial advice – thereby creating a link back to the intermediary.

Four questions intermediaries should ask themselves to build a digital-led business:

- Do you have a business profile on LinkedIn and Facebook, and do you regularly publish articles that would be of value to your clients?

- Are you using your website optimally to interact with existing and new clients and driving sufficient traffic? Does your website have a strong call to action and not only content?

- Do you offer your clients an e-signing capability?

- Are there aspects of your business – perhaps the admin side especially – that you could automate through a system or application?